Content

Use this guide to understand general information about Credit Card lifecycle.

1. Credit Card lifecycle overview

2. Key considerations

2.1. Key concepts

3. Credit Card payment lifecycle

4. Key characteristics

5. Credit Card processors and cutoff times

6. Void and refunds

2.1. Chargebacks handling

7. Additional related resources

1. Credit Card Overview |

Credit card transactions are electronic payment instructions initiated by a cardholder through a merchant, processed via the card networks (e.g., Visa, Mastercard, American Express) and the cardholder’s issuing bank. Unlike ACH transactions, credit card payments are typically authorized in real time, allowing immediate confirmation of fund availability, although settlement between financial institutions occurs afterward.

The lifecycle begins with the merchant submitting the transaction for authorization, during which the issuing bank approves or declines the payment based on credit availability, fraud checks, and account status. Approved transactions are then captured and submitted for clearing and settlement through the card network to the merchant’s acquiring bank. Settlement transfers funds from the issuing bank to the acquiring bank, while returns, chargebacks, and disputes are managed according to established network rules and timelines. As credit card transactions involve real-time authorization and a structured settlement process, allow faster processing compared to ACH transactions.

Risk management, fraud detection, and regulatory compliance are integral throughout the lifecycle, ensuring secure and reliable payment processing.

2. Key Considerations |

Credit card transactions are electronic payment instructions initiated by a cardholder through a merchant, processed via the card networks (e.g., Visa, Mastercard, American Express) and the cardholder’s issuing bank. Unlike ACH transactions, credit card payments are typically authorized in real time, allowing immediate confirmation of fund availability, although settlement between financial institutions occurs afterward.

The lifecycle begins with the merchant submitting the transaction for authorization, during which the issuing bank approves or declines the payment based on credit availability, fraud checks, and account status. Approved transactions are then captured and submitted for clearing and settlement through the card network to the merchant’s acquiring bank. Settlement transfers funds from the issuing bank to the acquiring bank, while returns, chargebacks, and disputes are managed according to established network rules and timelines. As credit card transactions involve real-time authorization and a structured settlement process, allow faster processing compared to ACH transactions.

Risk management, fraud detection, and regulatory compliance are integral throughout the lifecycle, ensuring secure and reliable payment processing.

KEY CONCEPTS:

- For chargeback or compliance purposes, merchants must retain transaction records, receipts, and authorization data.

- Credit card processing depends on the merchant’s acquiring bank, the card network, and the issuing bank. Network downtime, processing cutoffs, or settlement delays can affect fund availability.

- Temporary holds on cardholder funds can impact available credit and may remain until the transaction is captured or released, affecting customer account balance.

- Certain industries or transaction types carry higher risk for chargebacks or fraud, influencing processing requirements and reserve policies.

- Merchants may submit partial captures or adjustments after the initial authorization, which require proper reconciliation and can affect settlement amounts and reportig.

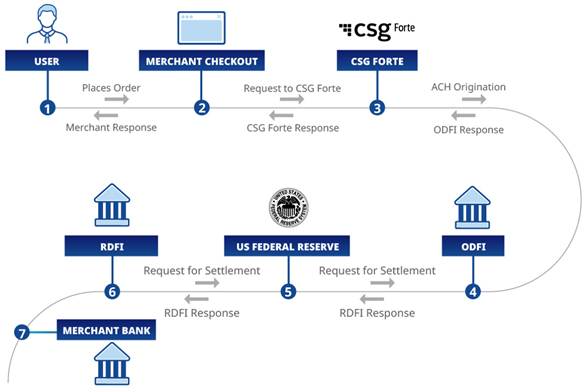

3. Credit Card Payment Lifecycle |

|

|

The credit card transaction lifecycle consists of the following stages:

Authorization | The customer provides card details, and the merchant submits a request for approval through a payment processor. |

Authentication and Approval | The issuing bank validates the transaction by checking card validity, available credit, and potential fraud indicators. The transaction is either approved or declined. |

Authorization Hold | If approved, the transaction amount is placed on hold on the customer’s credit line. Funds are not yet transferred. |

Clearing and Settlement | The merchant submits authorized transactions in a batch to the processor. The processor routes them through the card network to the issuing bank for settlement. |

Settlement Timing | ● Settlement files are typically generated around 1:00 AM, and merchants generally retrieve them around 5:00 AM, depending on processor configuration. Actual settlement timelines may vary according to processor schedules and merchant setup. |

Funding | The issuing bank transfers the funds (minus applicable fees) to the merchant’s acquiring bank. |

Customer Billing | The transaction appears on the customer’s credit card statement, and the customer repays the issuing bank according to their billing cycle. |

Disputes and Chargebacks (if applicable) | The customer may dispute the transaction, which may result in a chargeback and reversal of funds if the claim is validated. |

Credit card transactions involve four primary participants:

● Merchant: submits the transaction

● Processor: transmits and manages the transaction

● Card Network (Visa, Mastercard, etc.): routes authorization and settlement

● Issuing Bank: approves, declines, and funds the transaction

The processor sends authorization and settlement data to the network, which forwards it to the issuing bank for final approval and funding.

4. Key Characteristics |

|

|

Processing Timeframes | Credit card transactions involve real-time authorization and short settlement cycles. | ||

Transaction Types | Credit card transactions support multiple types that define how funds are handled: | ||

Type | Name | Description | |

10-SALE | Sale | Charges the customer’s credit card and sends the transaction for settlement. | |

11-AUTH ONLY | Authorization Only | Place a temporary hold on the cardholder’s funds without capturing them. | |

12-CAPTURE | Capture | Completes a previous AUTH ONLY transaction and sends it to settlement. | |

13 -CREDIT | Refund | Returns funds to the cardholder after a settled transaction. | |

14-VOID | Void | Cancel a transaction before settlement, preventing any funds from being captured. | |

15-PRE-AUTH | Pre-Authorization | Approves a charge initiated from another system or source and puts funds on hold temporarily. | |

Transaction Statuses | Transactions move through defined statuses during processing: | ||

Processing Nature | ● Real-time authorization model ● Batch-based settlement process ● Dependent on multiple parties:○ Processor: facilitate communication between systems ○ Card Network: routes transactions (e.g., Visa, Mastercard) ○ Issuing Bank: approves transactions and provides funds ● Subject to cutoff times and processor schedules ● Settlement and funding may be affected by:○ Processor risk reviews ○ Merchant risk category ○ High-volume or high-ticket processing ○ Issuer or network fraud review delays | ||

Dispute and Chargeback Risk | Credit card transactions are subject to disputes initiated by cardholders. | ||

5. Credit Card Processors and Cutoff Times |

|

|

CSG Forte maintains processing relationships with multiple credit card processors. Each merchant is associated with a specific processor, which facilitates transaction authorization, settlement, and funding. Applicable cutoff times:

PayPal

Processor | Cutoff |

Global Payments | 8:00 PM / 10:00 PM |

Nova / Elavon | 9:00 PM |

Vital / TSYS | 8:00 PM |

First Data | 10:00 PM |

Worldpay | 5:00 PM (unless configured otherwise) |

PayPal | 11:59 PM at the merchant's time zone |

● Processing relationships may be either directly managed by CSG Forte or supported through external processor teams, which may impact support and coordination efforts.

● Transactions submitted after the established cutoff time will be processed in the next business day’s batch, which may affect settlement and funding timelines.

6. Voids vs Refunds |

Action | When Used | Effect |

Void | Before settlement | Stops capture; preferred when possible. |

Refund | After settlement | Sends money back to cardholder. |

Chargeback Handling

If the customer disputes the charge (e.g., fraud or product issues), they can initiate a chargeback.

The bank investigates and may reverse the transaction, pulling the funds from the merchant’s account unless the merchant can prove the charge was valid.

7. Additional Topics for Further Reference |

|

|

Disputes

Topic | Context |

Limit Increase | A request to raise the approved ACH processing or funding limits for a merchant account. Limit increases are evaluated based on risk, transaction history, and funding exposure. |

Overview of transaction and verification codes used in CSG Forte payment processing, including status, response, return, settlement, AVS, and CVV codes. | |

This FAQ explains cutoff times for ACH and credit card transactions, including how they affect processing, settlement, returns, and funding timelines. It also covers processor-specific cutoffs, same-day ACH, midnight cutoff options, and expected funding delays. | |

CSG Forte’s PCI-DSS Program provides merchants with simple options to achieve PCI compliance, including a low-cost managed solution with guided validation, security scans, and data protection support. | |

Disputes | Documentation that supports a credit card dispute (chargeback). This documentation may be required to review, investigate, and resolve disputed card transactions in accordance with card network rules and compliance requirements. Note: Requests outcomes are determined by the requesting banks and applicable payment networks. CSG Forte acts only as an operational intermediary and does not control or make final decisions regarding their resolutions. |

Was this article helpful?

That’s Great!

Thank you for your feedback

Sorry! We couldn't be helpful

Thank you for your feedback

Feedback sent

We appreciate your effort and will try to fix the article